Quantitative trading is not just about building strategies. Picking the wrong market kills more quant projects than picking the wrong signal. A mean reversion strategy that works on US equities might blow up on crypto because the volatility is 3x higher. A trend following system profitable on commodity futures might sit idle for a year on EUR/USD because major currency pairs barely trend. The market itself determines what strategies survive: its rules, data quality, leverage structure, and trading hours all matter. This article breaks down the five major markets from a quant trader’s perspective.

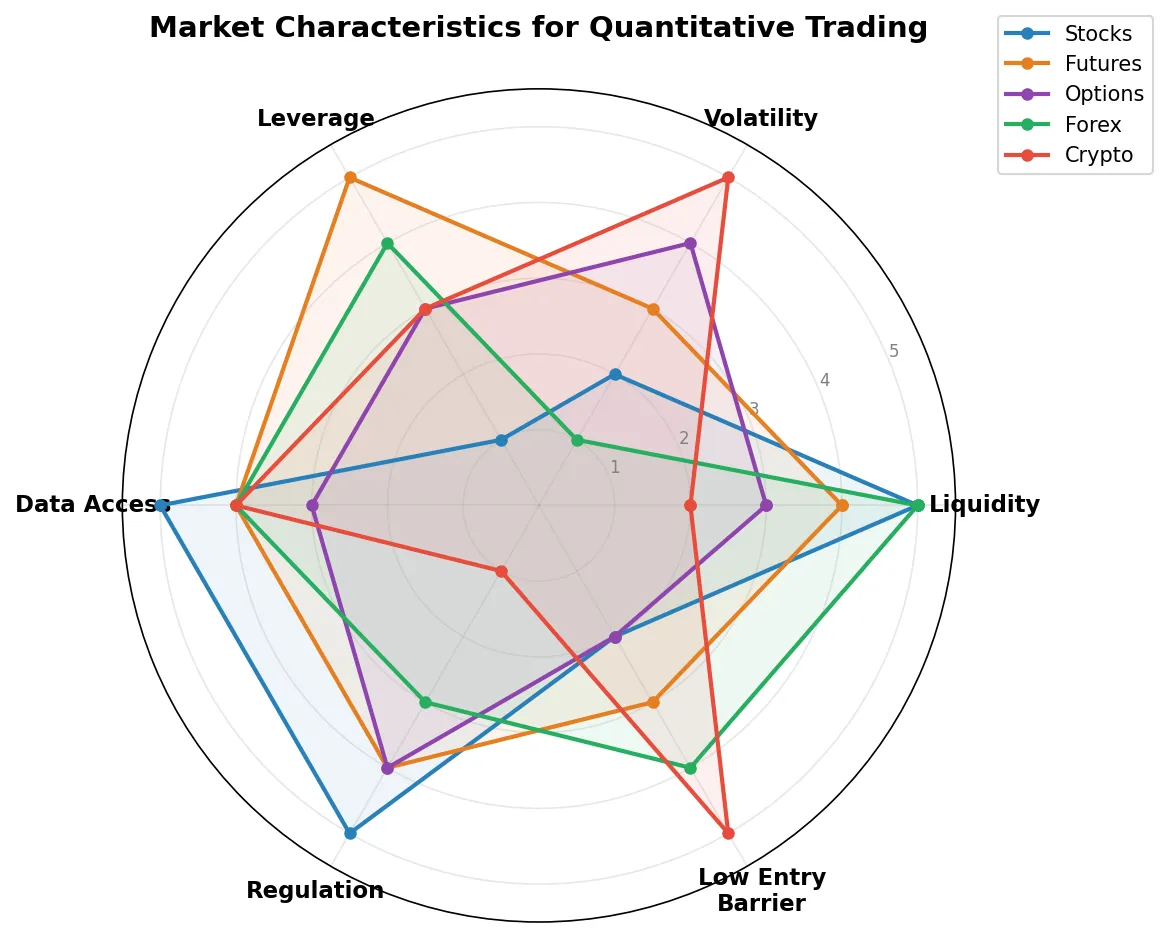

Five Markets at a Glance

A high-level comparison first, with details in the sections below.

| Stocks | Futures | Options | Forex | Crypto | |

|---|---|---|---|---|---|

| Trading hours | US: 6.5h; China A-shares: 4h | Near 24h (weekdays) | Same as underlying | 24h × 5 days | 24h × 7 days |

| Capital requirement | US: $25K PDT rule; China: a few thousand RMB | Margin deposit (thousands to tens of thousands) | Hundreds to thousands | Micro accounts from $100 | No minimum |

| Leverage | US: 2-4x; China A-shares: none (1x margin lending) | 5-20x (margin system) | Built-in (nonlinear payoff) | 30-50x (regulated); up to 500x offshore | 1-125x (perpetuals) |

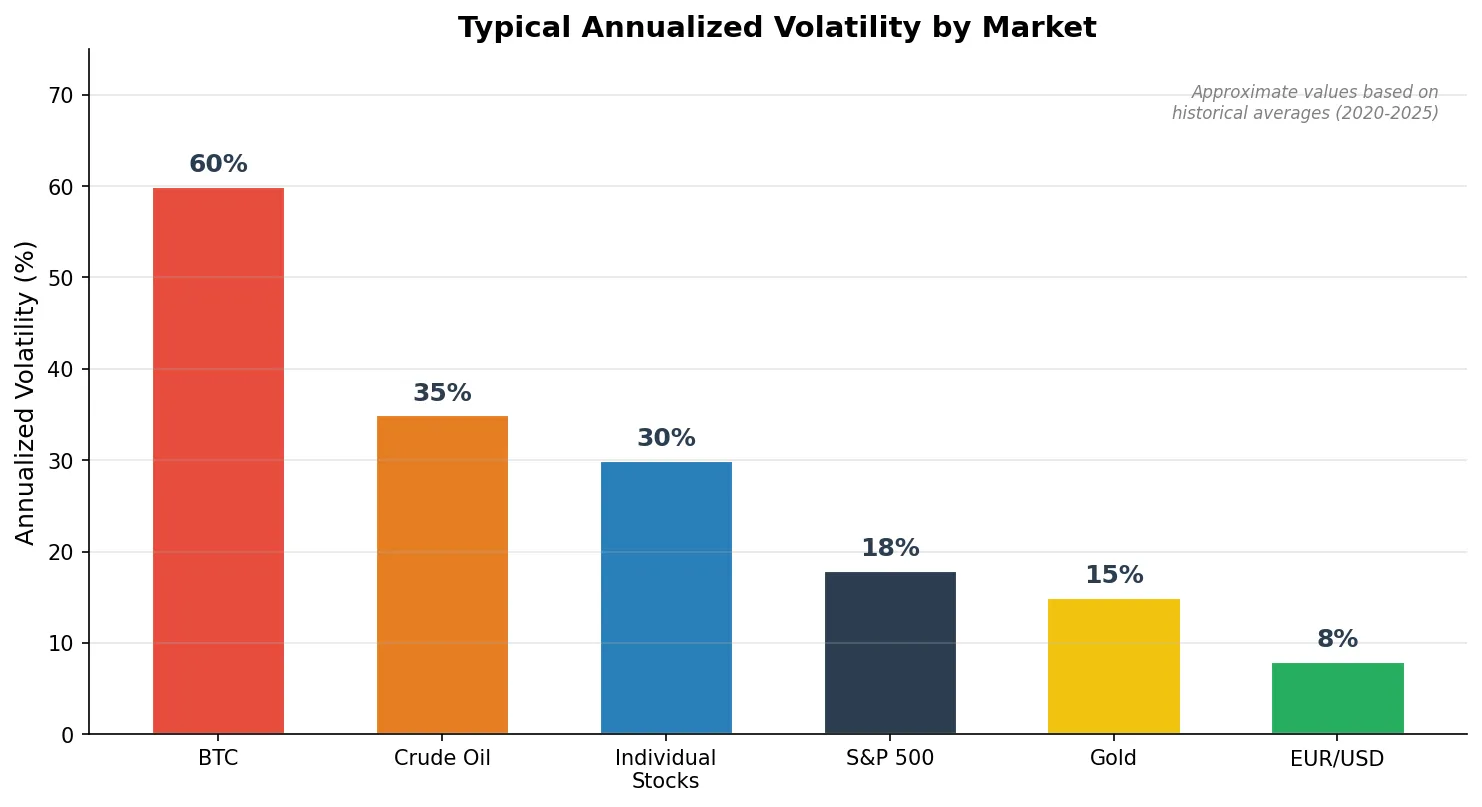

| Annualized volatility | Individual stocks ~30%, indices ~18% | Crude oil ~35%, steel rebar ~25% | Depends on underlying | Major pairs ~8% | BTC ~60% |

| Data/API ecosystem | Most mature | Mature | Moderate | Mature | Most open |

| Regulation | Strict | Strict | Strict | Moderate (retail brokers vary) | Immature |

| Best-fit strategies | Multi-factor, stat arb | CTA trend, spread arb | Volatility trading, hedging | Carry, mean reversion | Cross-exchange arb, trend |

Stocks

Stocks are where most quant traders start, for a simple reason: the data ecosystem is the richest and the academic research base is the deepest.

Trading rules vary dramatically by region. China A-shares enforce T+1 settlement: you cannot sell a stock the same day you buy it. This kills intraday strategies outright. US equities allow T+0 trading, but the SEC’s Pattern Day Trader (PDT) rule requires accounts with 4+ day trades per 5 business days to maintain at least $25,000 in equity. Below that threshold, US intraday strategies are off limits.

Factor research is the core battleground. Decades of academic work on Fama-French factors, momentum, quality, and low volatility have all been conducted on equity data. If you want to build multi-factor stock selection models, the infrastructure exists: Tushare and RiceQuant for A-shares, yfinance, Quandl, and Interactive Brokers API for US equities.

Liquidity is highly skewed. The top 300 A-share stocks trade hundreds of millions of RMB per day, but thousands of small-caps trade under 10 million. Statistical arbitrage strategies require liquid names; otherwise your orders move the price before your signal plays out.

Best-fit strategies: multi-factor stock selection (medium to low frequency, holding periods of days to weeks), statistical arbitrage (pairs trading, sector-neutral), event-driven (earnings, dividends, index rebalancing).

Futures

The defining feature of futures markets is margin-based trading: you post a fraction of the contract’s notional value (typically 5-15%) as collateral, gaining leveraged exposure. Same capital, larger position, proportionally amplified risk.

T+0, long and short. No restrictions on short selling, no T+1 settlement lock. Trend following strategies can flip from long to short at any time, unlike A-shares where you are stuck holding until the next day.

Contracts expire. Futures are not hold-forever instruments. Every contract has a delivery month. Trend strategies must “roll” positions from the expiring near-month to the next far-month contract before delivery. The near-far spread at roll time creates a cost (or occasional gain) that accumulates over years.

Strong inter-commodity relationships. Soybeans, soybean meal, and soybean oil share a physical crushing relationship. Steel rebar and iron ore are upstream-downstream. WTI and Brent crude are the same commodity from different regions. These natural correlations are the foundation for spread arbitrage and what distinguishes futures quant from equity quant.

Best-fit strategies: trend following (CTA, over 70% of global managed futures AUM), calendar spread arbitrage (same commodity, different delivery months), intercommodity spread arbitrage (related commodities). Position sizing typically uses ATR to normalize risk across instruments.

Options

Options are the most “mathematical” of the five markets. While stocks and futures have linear payoffs (a 1% move earns 1%), options have nonlinear payoffs: a call option might return 50% when the underlying rises 5%, but lose its entire premium from time decay if the underlying goes nowhere.

Greeks are the language of options quant. Delta measures sensitivity to the underlying price, Gamma measures how fast Delta changes, Theta is daily time decay, and Vega captures the impact of implied volatility shifts. Without a working understanding of Greeks, options quant is a non-starter.

Volatility itself is a tradable asset. Stocks and futures trade “direction” (up or down). Options can trade “volatility” (whether the magnitude of moves will be large or small). Selling a straddle profits when implied volatility exceeds realized volatility; buying a straddle bets on a large move in either direction. This is a dimension that no other market offers.

Liquidity concentrates in a few names. SPY, QQQ, and AAPL options trade with penny-wide spreads. Most individual stock options have bid-ask spreads wide enough to eat your edge. In China, 50ETF options and CSI 300 options are the liquid names, and not much else.

Best-fit strategies: volatility trading (long/short implied vol), Delta hedging (neutralize directional risk, isolate vol exposure), premium selling (sell OTM options to collect theta), structured strategies (iron condors, butterfly spreads).

Forex

Forex is the world’s largest market by daily volume: $7.5 trillion per day according to the 2022 BIS survey. For quant traders, the practical benefit of that liquidity is low execution cost: EUR/USD spreads are typically under 1 pip (0.0001), meaning a $100,000 notional trade costs less than $10 in spread.

24-hour continuous trading. From Monday morning in New Zealand to Friday close in New York, the market runs nonstop. Asia, Europe, and Americas sessions overlap seamlessly. For quant systems, this means overnight gaps are essentially nonexistent (except over weekends), and stop orders almost always fill near the intended price.

Major pairs trend weakly. EUR/USD and USD/JPY are driven by central bank policy, trade balances, and interest rate differentials. Most of the time they oscillate within ranges. Trend following strategies on major FX pairs consistently underperform compared to commodity futures. Mean reversion strategies have more fertile ground here.

Leverage can be extreme. Post-ESMA (EU) and ASIC (Australia) reforms cap retail FX leverage at 30:1 on major pairs. The US (NFA) caps at 50:1. Offshore and unregulated brokers still offer 200:1 or 500:1. EUR/USD daily volatility is about 0.5%. At 100x leverage, that translates to 50% daily equity swings. Without strict position sizing, blowing up is a matter of when, not if.

Retail broker risk. Unlike stocks and futures (where brokers are strictly regulated custodians), many retail FX brokers operate as dealers: your counterparty is the broker itself. Some engage in slippage manipulation, requoting, or even blocking withdrawals. Stick to brokers regulated by the FCA (UK), NFA (US), or ASIC (Australia).

Best-fit strategies: carry trade (long high-yield currencies, short low-yield currencies, earning the interest rate differential), mean reversion (range-bound trading on major pairs), macro factor models (using economic data to forecast exchange rate direction).

Crypto

The crypto market is barely a decade old, and the rules are still being rewritten.

24/7/365. No open, no close, no holidays. BTC trades at 3 AM on Christmas. This places the highest operational demands on quant infrastructure: servers cannot go down, strategies must handle extreme moves at any hour. The upside is no “overnight risk” definitional problem. The downside is no natural pause.

Volatility dwarfs all other markets. BTC’s annualized volatility sits around 60% long-term. Altcoins routinely move 20-30% intraday. Trend following strategies have a natural edge in crypto: when trends form, they are enormous. The flip side: stops set too tight get triggered by normal noise.

The most open API ecosystem. Nearly every major exchange (Binance, OKX, Bybit) offers free REST and WebSocket APIs. Tick-level data, order placement, account queries: a few lines of Python will do it. Compare this to equities (IB API requires an account and monthly fees) or futures (CTP interface requires broker approval in China), and crypto’s barrier to entry for automated trading is the lowest.

Exchange risk is unique to crypto. FTX collapsed in 2022 and user assets vanished overnight. Mt. Gox, Luna/Terra, and others preceded it. Stocks sit in regulated brokerage custody with investor protection funds. Crypto exchanges offer none of that. Distributing funds across multiple exchanges and never keeping more on any exchange than your strategy actively needs is a basic survival rule.

Regulatory uncertainty. Government attitudes toward crypto range from outright bans (mainland China) to full embrace (El Salvador). Policies shift without warning. When China banned crypto trading in 2021, exchanges and mining operations relocated overnight. Regulatory risk cannot be hedged by any strategy.

Best-fit strategies: cross-exchange arbitrage (same asset priced differently on different exchanges, wider spreads than in traditional markets), funding rate arbitrage (perpetual contract funding rates vs. spot), trend following (high volatility environment suits momentum), market making (providing liquidity on illiquid altcoins for spread capture).

How to Choose a Market

There is no “best market for quant trading.” The right choice depends on specific constraints.

| If you want to… | Best market | Why |

|---|---|---|

| Build factor models | Stocks | Deepest data and research base |

| Run trend following | Futures, Crypto | High volatility, unrestricted shorting |

| Trade volatility | Options | Only market with direct vol exposure |

| Capture arbitrage | Crypto, Futures | Crypto has wide cross-exchange spreads; futures have strong inter-commodity links |

| Start with low capital | Crypto, Forex | No minimum or very low minimum |

| Go high-frequency | Crypto, Futures | Open APIs, T+0, low fees |

A few dimensions to consider:

Capital requirements. Crypto has virtually no minimum. Forex micro accounts start at $100. Futures require margin deposits of a few thousand dollars or more. A-shares have no hard minimum but tiny accounts lose too much to fees. US intraday equity trading has a hard $25,000 PDT floor.

Strategy fit. Trend following works best on futures and crypto, where volatility is high and shorting is unrestricted. Factor-based stock selection benefits from equity markets’ deep data and research base. Volatility trading only exists in options markets. High-frequency or arbitrage strategies favor crypto’s open APIs and market inefficiencies.

Risk profiles. Each market has a different “way to die.” Stocks can suffer systemic drawdowns but individual positions rarely go to zero. Futures amplify losses through leverage, and margin calls force liquidation at the worst time. Options sellers face tail risk: a black swan event can produce losses 50x the premium collected. Crypto risks include exchange failures and regulatory shocks. Understanding each market’s failure mode matters more than understanding its profit mechanism.

Depth over breadth. Every market has its own microstructure, data quirks, and strategy ecosystem. Switching markets carries a steep learning curve. Pick one, run paper trading for at least three months before going live. For strategy evaluation metrics (Sharpe ratio, max drawdown, Calmar ratio), see the quant metrics guide.