0DTE options (Zero Days to Expiration) are option contracts that expire on the same day they trade. In 2022, CBOE filled out the SPX expiration calendar so that contracts expire on every weekday (Tuesdays added in April, Thursdays in May), moving 0DTE from a niche product into mainstream trading. Cboe public materials report that 0DTE contracts account for more than half of daily SPX option volume, with the share continuing to rise through 2024-2025.

Public discussion of 0DTE tends to cluster at two extremes: social-media narratives of rapid wealth, and warning labels of indiscriminate risk. This article takes neither stance. The aim is to examine 0DTE as a financial instrument: its pricing mechanics, the evolution of Greeks during the final trading day, the payoff structures faced by the main participant types, and the empirical findings of existing academic work on the realised return distribution of retail buyers. With these in hand, a reader can form an independent view of whether the instrument fits their objectives.

What 0DTE Options Are and Why They Exploded in 2023

The CBOE timeline for SPX expirations is worth committing to memory:

| Year | Event |

|---|---|

| Pre-2005 | SPX options were monthly only |

| 2005 | Friday weekly expirations introduced |

| Feb / Aug 2016 | Wednesday, then Monday weekly expirations added |

| Apr / May 2022 | Tuesday and Thursday added; every weekday now expires |

| 2023-2024 | 0DTE > 50% of daily SPX volume |

Retail participation has risen sharply alongside this volume growth. Zero-commission brokers (Robinhood, Webull) lowered the barrier to entry, and the asymmetric payoff of options aligns well with the propagation pattern of social-media content. Cboe public materials (including talks by chief strategist Mandy Xu in 2024-2025) describe retail as a meaningful share of 0DTE flow; the exact figure varies with how “retail” is defined. The remainder reflects dealer hedging and institutional delta-one position management.

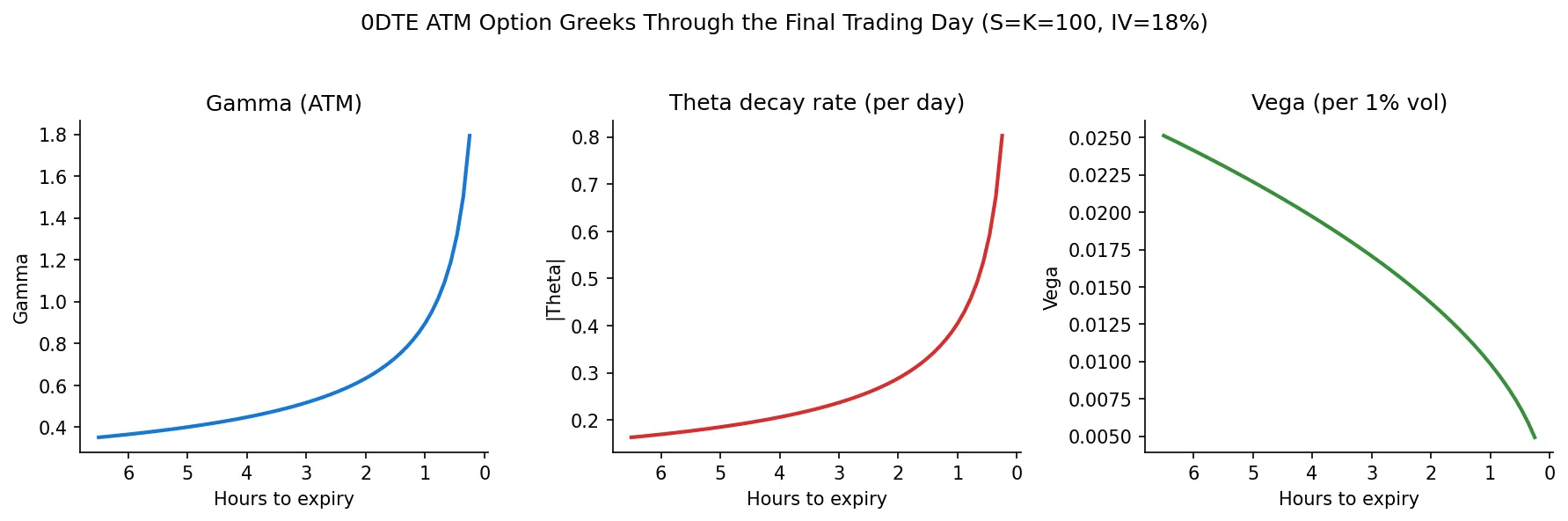

The Extreme Greek Behavior of 0DTE Options

Option Greeks measure price sensitivity to various factors. On 0DTE options, those sensitivities enter a very different regime from monthly contracts.

The Black-Scholes Gamma for an at-the-money option is:

$$\Gamma = \frac{\phi(d_1)}{S \sigma \sqrt{T}}$$where \(\phi\) is the standard normal density and \(T\) is time to expiry in years. Note the \(\sqrt{T}\) in the denominator: as \(T \to 0\), Gamma diverges. This is not a mathematical curiosity. It is what happens on a real trading day.

The chart below shows ATM Gamma, Theta, and Vega evolving across the final trading day for a stylised 0DTE call (S=100, K=100, IV=18%, r=5%, Black-Scholes):

Three things change non-linearly:

- Gamma spikes: at six hours to expiry ATM Gamma is moderate; at thirty minutes to expiry it has multiplied several times over. A one-dollar move in the underlying can take Delta from 0.5 to 0.9 and back to 0.3 within minutes.

- Theta accelerates: time decay is not linear. In the final hour, the decay rate runs several times higher than at the morning open, and rises further in the last few minutes. “Goes to zero in the last hour” is a real physical process, not folklore.

- Vega approaches zero: the remaining time is too short for implied vol changes to matter much. On 0DTE, IV is no longer a meaningful pricing dimension; realised directional moves dominate.

Real markets are messier than Black-Scholes. BS assumes constant vol, no jumps, continuous hedging; on 0DTE all three break. End-of-day implied vol often rises because dealers demand a risk premium for the remaining hours, a phenomenon discussed in the SSRN literature under the “end-of-day variance risk premium” theme.

Time Value Collapses Non-Linearly on the Final Day

Plot ATM option price against holding time and you get a concave curve. Ignoring rates, the ATM option price is approximately:

$$C_{ATM} \approx 0.4 \cdot S \cdot \sigma \cdot \sqrt{T}$$The \(\sqrt{T}\) relationship determines the shape of decay. If a contract is worth 1.0 at six and a half hours to expiry, it follows roughly:

| Time to expiry | \(\sqrt{T}\) ratio | Remaining value | Value lost in this segment |

|---|---|---|---|

| 6.5 h | 1.000 | 1.000 | — |

| 3 h | 0.679 | 0.679 | 32% |

| 1 h | 0.392 | 0.392 | 29% |

| 30 min | 0.277 | 0.277 | 11% |

| 10 min | 0.160 | 0.160 | 12% |

| 1 min | 0.051 | 0.051 | 11% |

This explains why ATM contracts approach zero rapidly near the close. A buyer holding ATM into the closing bell faces accelerating time decay, and any reliance on directional movement to outrun decay imposes a high required hit rate.

If the underlying is flat in the last hour, an ATM option loses close to half of its remaining value in the final 30 minutes. This is not the result of any directed activity; it is a consequence of the \(\sqrt{T}\) decay term.

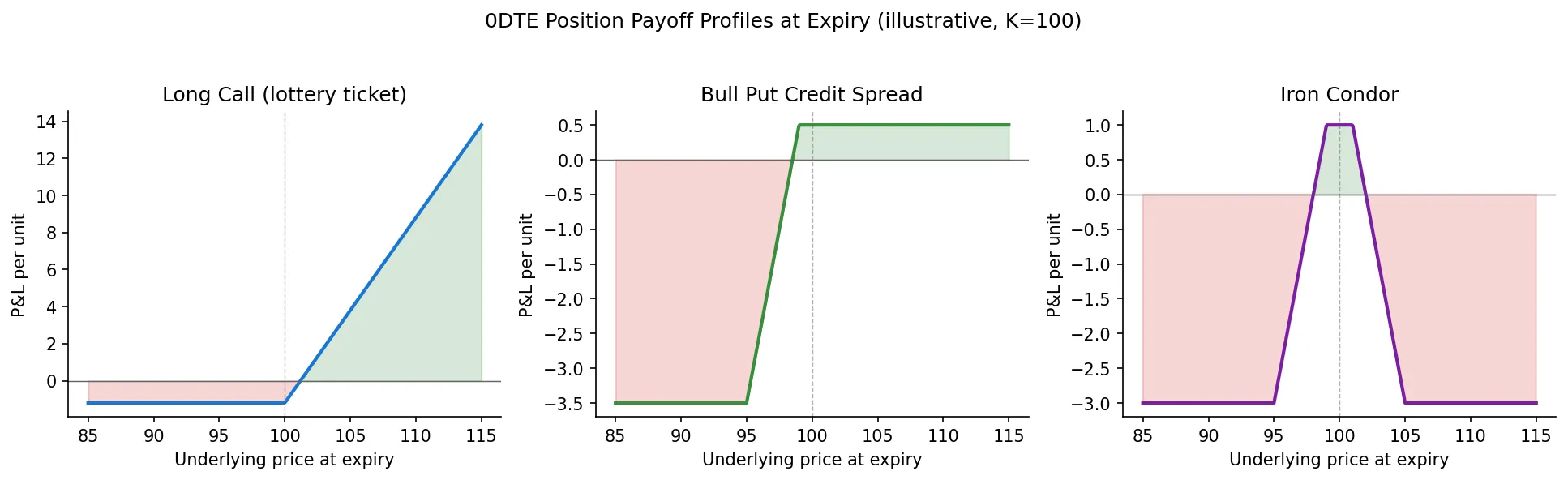

Three Player Types and Their Payoff Profiles

The 0DTE market has roughly three types of participants.

Buyer (lottery ticket): simply buying calls or puts. Maximum loss is the premium, theoretical upside is unbounded. This is the most common retail expression. The appeal is the asymmetric “bet a hundred to win ten thousand” payoff. The problem is hit rate, covered in the next section.

Credit spread (e.g., bull put spread): sell a near-ATM option, buy a further OTM option as protection. The position opens with a net credit. Maximum profit is that credit; maximum loss is the strike width minus the credit. Typical risk-reward ratios run 1:3 to 1:5, meaning you stand to win one unit on a quiet day and lose three to five units on a tail event.

Iron Condor / Iron Butterfly: combine a bear call spread and a bull put spread to bet the underlying stays inside a range. On calm days the win rate is high. When the range breaks, losses scale structurally. February 5, 2018 (Volmageddon) and August 5, 2024 (yen carry unwind) wiped out months of accumulated profits for many short-vol books in a single session.

None of these payoffs is “better” than the others. Buyers pay premium for convexity; sellers collect premium for selling convexity; market makers hedge both sides and earn the spread. They are different views of the same balance sheet.

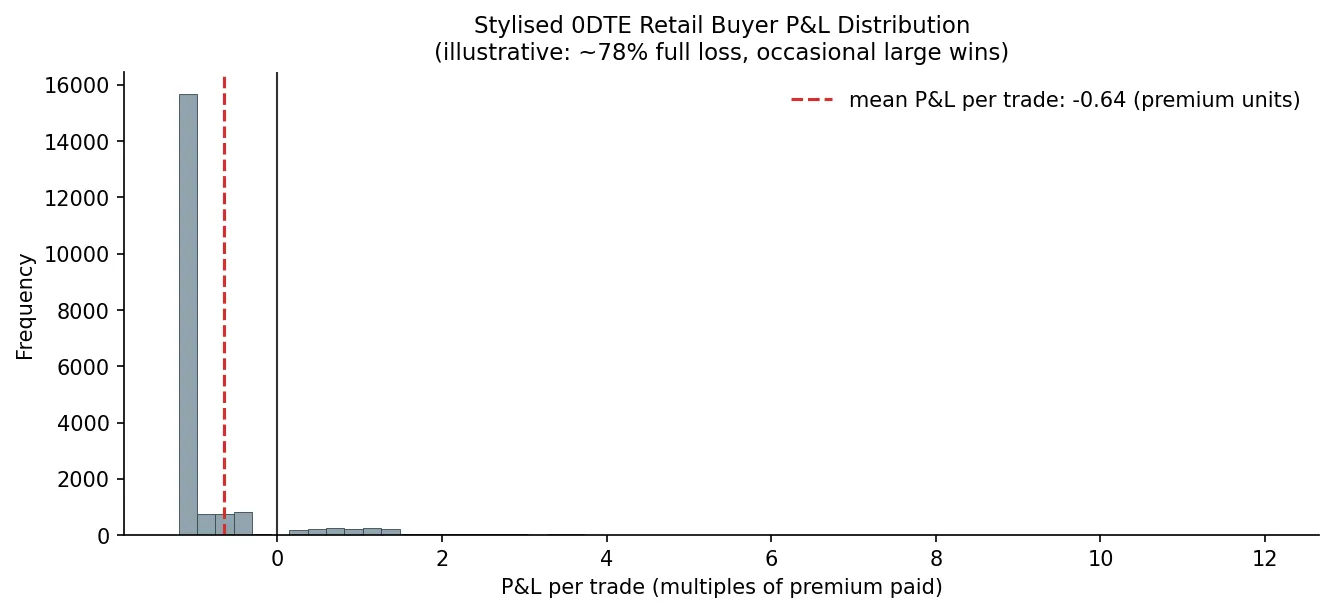

What the Retail P&L Distribution Actually Looks Like

The unavoidable question: do 0DTE buyers make money on average?

Published academic literature says no. Bryzgalova, Pavlova, and Sikorskaya in their 2023 paper Retail Trading in Options and the Rise of the Big Three Wholesalers analysed actual fills in US retail option accounts from 2019-2021. Key findings:

- Retail option traders are net losers in aggregate, primarily through bid-ask spread, time decay, and adverse selection by high-frequency market makers

- Short-dated expirations (which subsume early 0DTE flow) showed the worst loss rates

- Per-trade expected returns were negative, but the distribution was right-skewed; rare large winners maintained the gambling appeal

JPMorgan, Goldman, and other sell-side desks have published 2023-2024 strategy notes pointing in the same direction: 0DTE retail buyers have been net losers over the sample windows examined, with sharply right-skewed distributions and median outcomes near full premium loss. Reported headline numbers vary widely across notes, and depend heavily on sample selection and methodology.

The chart below illustrates the qualitative shape (based on the literature, not real samples):

The shape of this distribution matters more than its exact numbers: the bulk of trades lose all or nearly all of the premium, a small minority post modest gains, and a thin tail produces multi-bagger payoffs. The thin tail is heavily amplified on social media, which can distort perception of the underlying distribution. Specific percentages vary substantially across samples, underlyings, and definitions of “trade”.

The mean (red dashed line) sits in negative territory. In pure expectation terms, replicating the average participant produces a long-run loss. Producing positive expected value requires simultaneous outperformance on hit rate, timing, and identification of mispriced contracts; each of these is individually a difficult problem.

Who Is Actually on the Other Side of Your Trade

When you buy a 0DTE call, the seller is usually not another retail trader. It is a market maker (Citadel Securities, Susquehanna, Optiver, Jane Street, and a few others). Once they sell the call, they immediately hedge by buying the corresponding amount of the underlying stock or futures, a process called dealer Gamma hedging.

Because 0DTE Gamma is enormous (see earlier section), the dealer’s hedging itself moves the underlying. The mechanism:

Underlying drops → dealer's short call Delta decreases

→ dealer sells underlying to re-hedge

→ push price further down

→ short-term self-reinforcing decline (reverse gamma squeeze)

This is why SPX often shows seemingly inexplicable rapid moves in the final 30 minutes. There is a dedicated industry indicator, GEX (Gamma Exposure), that tracks dealer net gamma positioning, and academic work has documented systemic intraday volatility changes in SPX after 0DTE was introduced.

The practical implication: the bid-ask spread, slippage, and momentary liquidity contractions a participant encounters are not random, but the product of a structured counterparty network. That network has systemic advantages in data access, model iteration speed, and hedging cost. This does not imply that retail participants must lose; it does mean any intuition along the lines of “there exists a simple, replicable, reliably profitable approach” is distant from the structural facts of the market.

Common Misconceptions

Ranked by frequency, the most common misconceptions:

“Selling premium is a sure thing because of time decay”

Sellers earn small amounts on most days and incur large losses on rare days. An Iron Condor with a 1:3 to 1:5 risk-reward profile requires a 75-83% hit rate to break even, and the “stays in range” probability is already discounted in the implied vol surface. In a liquid underlying, premium levels mean-revert toward equilibrium pricing, and a structural “free lunch” does not persist.

“Iron Condors have limited risk, so they are safe”

Limited is not the same as small. The maximum loss is typically 3-5x the credit collected; a single adverse session can erase months of profit. “Limited” describes the mathematical bound, not the position’s compatibility with a given account size.

“It’s just a small bet, the worst case is losing the premium”

True per trade, false across many trades. Repeated 100% premium losses compound geometrically. Producing positive expected value out of this distribution requires rare large gains to offset accumulated losses, and such gains are empirically rare and difficult to forecast.

“I have an information / TA / AI edge that can beat the market”

Public technical analysis at minute-level on SPX has been examined in decades of literature, and most claims have failed out-of-sample testing. Machine learning models that produce stable alpha are typically absorbed by well-capitalised funds. The 0DTE counterparty pool consists of top-tier market makers; the assumption that an individual retains a durable information or modelling advantage requires stronger evidence than is generally available.

Further Reading

If you want to go deeper after the above:

- Greeks fundamentals: Option Greeks Complete Guide covers the math and intuition for Delta/Gamma/Theta/Vega/Rho

- Second-order Greeks: Second-order Option Greeks on Vanna, Charm, and Volga, central to understanding dealer hedging flow

- Position sizing: Kelly Criterion for Position Sizing on why no sizing rule rescues a negative-expectation game

- Backtest hygiene: Common Backtesting Pitfalls for anyone who wants to validate a 0DTE idea without fooling themselves

Primary and industry sources:

- Bryzgalova, Pavlova, Sikorskaya (2023). Retail Trading in Options and the Rise of the Big Three Wholesalers. SSRN.

- Cboe Global Markets public talks and research notes on 0DTE volume and participant mix (Mandy Xu et al., 2024-2025).

- SSRN papers tagged with “0DTE”, “end-of-day variance risk premium”, and “dealer gamma” provide useful entry points for further reading.

The mechanics of 0DTE options are neutral: high Gamma, low residual Theta, and high turnover define a particular type of instrument. Whether the mechanics are well understood and whether the instrument is profitable for a given participant are two separate questions. This article covers the former. The latter depends on the participant’s capital base, risk tolerance, information access, modelling capacity, and an honest assessment of their own decision process.